Traveler deciding whether to add travel insurance during online booking

Is Travel Insurance Worth It for Your Next Trip?

Content

Content

You've clicked "book now" on that dream vacation. Before you finish checking out, a pop-up asks if you want trip protection. Maybe it's $287 to protect a $4,200 cruise. Maybe it's $68 for a $1,200 weekend getaway. Either way, you're stuck wondering if this extra charge actually makes sense.

Here's the thing: some trips desperately need insurance coverage. Others don't. A family spending $12,000 on a Mediterranean cruise six months from now? They'd be foolish to skip it. Someone driving two hours away for a flexible weekend? That's throwing money away.

Most policies run between 4-10% of what you're spending on the trip itself. So that $5,000 vacation might need another $200-$500 for protection. Whether you should pay depends on factors most travelers never consider before clicking "yes" or "no."

What Travel Insurance Actually Covers

Think of travel insurance as a safety net with multiple layers. Each layer catches a different type of disaster. Knowing exactly what you're paying for helps you decide if the protection matches your actual risks.

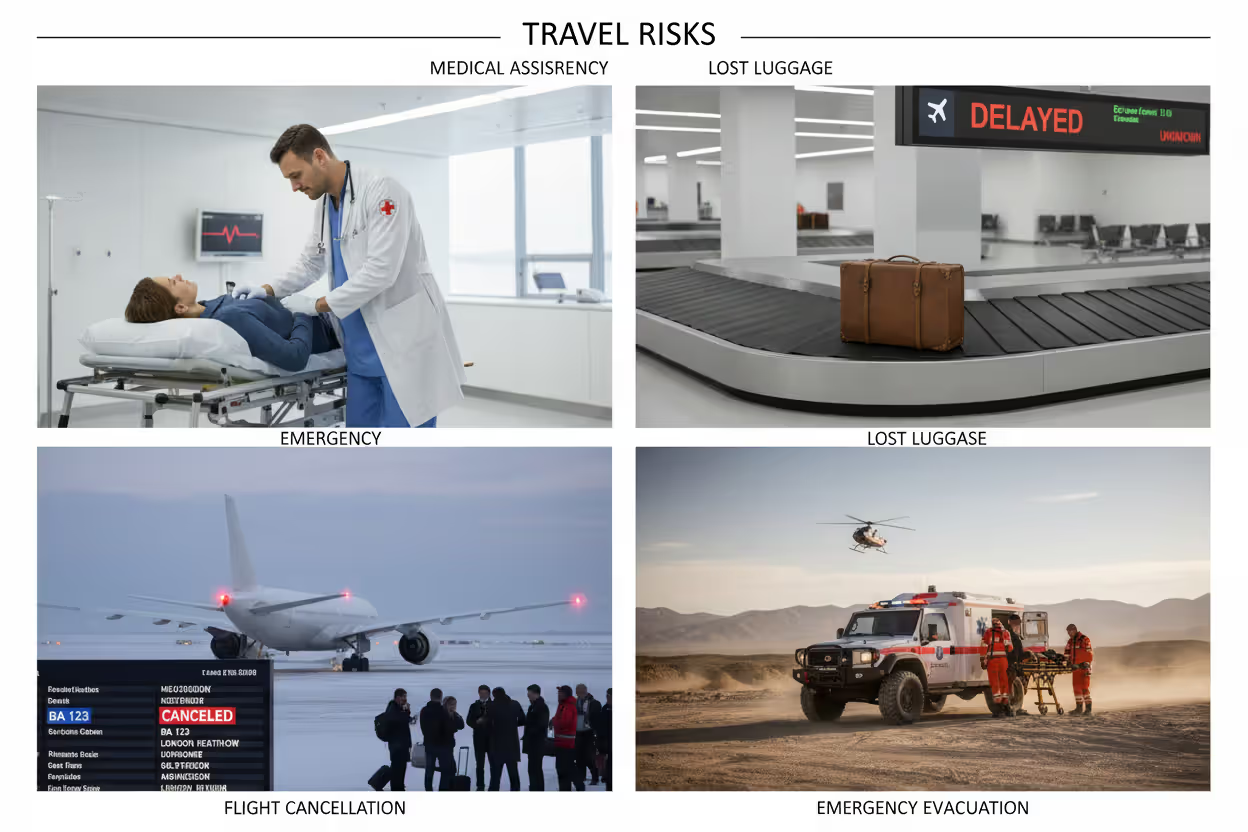

Trip cancellation and interruption protection gives you back money spent on non-refundable reservations when you can't travel. Covered situations usually include unexpected illness, injury to you or close family members, death, jury duty, your house flooding or catching fire, and sudden mandatory work obligations. Just changed your mind about going? That won't fly with basic coverage. Want that flexibility? You'll need to upgrade to "cancel for any reason" protection, which typically runs 40-60% higher.

Emergency medical protection handles doctor bills, hospital charges, and medications when you're traveling. This becomes critical outside the United States, where your regular health insurance often stops working or provides virtually nothing. You'll find policies offering anywhere from $50,000 to $500,000 in medical expense coverage. Sounds like plenty until you realize that getting airlifted off a mountain by helicopter can drain $30,000 from that limit in a single afternoon.

Author: Samantha Lowell;

Source: visitmuseumcampussouth.com

Emergency medical evacuation gets you to a hospital that can actually treat your condition, or flies you home if needed. Picture getting seriously hurt in rural Thailand. The local clinic can't handle your injuries. Flying you to Bangkok or back to the US on a medical transport? That bill can hit $100,000 or more—which is why this coverage matters for remote destinations.

Baggage loss and delay protection reimburses you when airlines lose your luggage, someone steals it, or it gets damaged. You'll also get money for essential purchases when bags show up late. Don't expect miracles here—most policies cap this at $1,000-$3,000 total, with individual item limits around $250-$500. Pack a suitcase full of luxury goods and you'll still take a loss.

Travel delay protection starts paying out when departures get pushed back for covered reasons like weather, equipment problems, or strikes. You'll typically need to wait 6-12 hours before this kicks in, then you can get reimbursed for hotel rooms, meals, and essential items up to around $500-$1,000.

Comprehensive policies bundle all these protections together. Single-issue plans focusing only on medical emergencies or trip cancellation cost less but leave you exposed. Whether that bundled protection delivers value depends entirely on what could actually go wrong on your specific trip.

Author: Samantha Lowell;

Source: visitmuseumcampussouth.com

How Much Does Travel Insurance Cost

Insurance companies calculate your premium based on several factors: total trip cost, how old you are, where you're going, and which coverage level you select. Industry averages land somewhere between 5-7% of total trip cost, though your actual quote might swing higher or lower.

Let's say you're 35 years old booking a $3,000 Caribbean getaway. Comprehensive coverage might run $150-$210. That exact same trip for someone who's 70? Expect $300-$450 because medical risks climb with age. Your destination shifts the price too—European coverage generally costs less than protection for countries where medical evacuations get complicated and expensive.

Here's how the math typically shakes out:

| Trip Cost | Typical Insurance Cost | Coverage Amount | Worth It? |

| $1,000 | $50-$80 | Trip cancellation up to $1,000, medical coverage to $50,000 | Maybe—depends heavily on refund policies and where you're headed |

| $3,000 | $150-$240 | Trip cancellation up to $3,000, medical coverage to $100,000 | Usually yes for international trips with money locked in |

| $5,000 | $250-$400 | Trip cancellation up to $5,000, medical coverage to $250,000 | Strong case for most travelers |

| $10,000+ | $500-$1,000+ | Trip cancellation matching trip cost, medical coverage to $500,000 | Absolutely essential when this much money's at stake |

Upgrading to "cancel for any reason" adds that 40-60% premium bump, but you can bail for literally any reason and get back 50-75% of what you prepaid. That $3,000 vacation might cost $240-$336 to protect with this flexibility built in.

Pre-existing medical condition waivers let you claim coverage for health issues you had before buying the policy. The catch? You must purchase within 10-21 days after making your first trip payment, and you need to insure everything you've prepaid. Meeting these requirements usually doesn't cost extra, but the timing window stays firm.

Annual multi-trip policies make sense for frequent travelers. Paying $300-$600 yearly covers unlimited trips lasting up to 30-45 days each. Take three or more trips per year and this beats buying separate policies every time.

When Travel Insurance Is Worth Buying

Certain trip characteristics flip insurance from "maybe" to "absolutely." These situations create scenarios where relatively small premiums protect against disproportionately massive losses.

International travel sits at the top of this list. Your U.S. health insurance probably won't help you abroad—or it'll provide such limited coverage that you might as well have nothing. Break your leg skiing in Switzerland and need surgery? That bill could land between $25,000-$40,000 out of your own pocket. This scenario alone justifies insurance for most international trips.

Expensive prepaid bookings create classic insurance situations. You've committed $8,000 to an African safari nine months before departure. Life throws curveballs in nine months. Someone gets sick. Your parent needs unexpected care. Work explodes. Spending $400-$600 on insurance protects that entire $8,000 investment against dozens of potential problems.

Cruises demand special attention because cruise lines penalize cancellations harshly. Back out 60 days before sailing and you might lose half your fare. Cancel within 30 days and you'll forfeit everything. That $6,000 cruise booking carries real financial risk that $300-$420 in insurance directly addresses.

Adventure activities like backcountry skiing, scuba diving, or mountain climbing boost injury probability and often require costly evacuations from places helicopters can barely reach. Standard policies frequently exclude these activities entirely, forcing you to buy specialized coverage. Planning a week of backcountry skiing in Colorado? That helicopter evacuation coverage stops being optional.

Health concerns make insurance valuable even on shorter trips. If you or someone traveling with you manages diabetes, heart problems, or respiratory issues, medical coverage and trip cancellation protection provide genuine peace of mind. The pre-existing condition waiver becomes critical in these situations.

Remote destinations with limited medical facilities make evacuation coverage essential rather than optional. Traveling to rural Central America, Africa, or Asia means the nearest competent hospital could sit hours away by air ambulance. Medical evacuation coverage that seems excessive for a Paris trip becomes crucial when you're headed to rural Peru.

Group travel multiplies cancellation risk through simple math. Four family members traveling together means four separate chances someone gets sick or injured before departure. The more people in your group, the higher the statistical probability you'll actually need that cancellation coverage.

Author: Samantha Lowell;

Source: visitmuseumcampussouth.com

When You Can Skip Travel Insurance

Insurance makes perfect sense for high-stakes, high-cost situations. Plenty of trips don't meet that threshold though. Recognizing when you can safely skip coverage keeps money in your pocket without adding real risk.

Domestic road trips with flexible arrangements need minimal protection. You're driving your own vehicle, staying in hotels that allow cancellation, and your regular health insurance follows you across state lines. A weekend trip three hours away doesn't justify spending $75-$100 on insurance. Exception: you've locked in non-refundable vacation rentals or event tickets worth serious money.

Fully refundable bookings eliminate insurance's main benefit. Your hotel lets you cancel free until 24-48 hours before check-in. Your flight is refundable, or you booked with miles. You're not actually risking money here. Buying insurance to protect refundable bookings doesn't make mathematical sense.

Strong credit card coverage might already protect you adequately. Premium travel cards often include trip cancellation protection (usually $1,500-$10,000 per trip), travel delay reimbursement, baggage delay coverage, and rental car protection. Check your card benefits carefully before buying duplicate protection. One important catch: you must charge your entire trip to that specific card to trigger these benefits.

Short, inexpensive trips don't justify the cost-benefit calculation. A $600 weekend getaway two months out carries minimal financial risk. Even if you must cancel, losing $600 hurts less than losing $6,000. Insurance might cost $30-$50, which means spending 5-8% of your trip cost for relatively low absolute dollar risk.

Last-minute bookings shrink the time window where cancellation becomes necessary. Book a trip departing in two weeks and you're only exposed to two weeks of potential illness, emergencies, or changed circumstances. Compare that to six months of exposure when you book far in advance.

Travel to countries with excellent public healthcare reduces medical coverage importance. Canada, most European countries, Australia, and Japan operate high-quality medical systems where even paying out-of-pocket stays relatively reasonable. You'll still want evacuation coverage for remote areas within these countries, but basic medical coverage becomes less critical.

Author: Samantha Lowell;

Source: visitmuseumcampussouth.com

Common Travel Insurance Mistakes That Waste Money

Buying travel insurance doesn't automatically mean you're properly protected. These mistakes leave travelers paying premiums without getting appropriate value in return.

Buying the wrong coverage level happens when people chase the cheapest policy without checking what they're actually getting. A $25,000 medical coverage limit might look adequate until you need emergency surgery in a foreign country. Similarly, accepting minimal baggage limits when you're carrying $5,000 in camera equipment sets you up for disappointment. Match your coverage limits to your actual financial exposure.

Duplicate coverage means paying for protection you already own. Your health insurance might actually cover emergency medical care internationally—have you checked? Your credit card might provide trip cancellation coverage. Your homeowners policy might already cover lost baggage. Before buying comprehensive travel insurance, audit your existing coverage and identify actual gaps. You might only need medical evacuation coverage instead of a full policy.

Ignoring exclusions leads directly to denied claims. Standard policies exclude pre-existing medical conditions unless you purchase a waiver within the required timeframe. They exclude injuries from extreme sports unless you specifically add adventure coverage. They won't cover cancellations because you're scared to travel or simply changed your mind—you need "cancel for any reason" for those situations. Actually read that 20-page policy PDF, not just the marketing brochure.

Buying from tour operators or cruise lines costs more while delivering less coverage. These companies mark up insurance heavily and offer policies with restrictive terms. Third-party insurers provide better coverage at lower prices consistently. That tour operator charging $400 for coverage? An independent insurer probably offers superior protection for $250.

Waiting too long to purchase locks you out of valuable benefits. Pre-existing condition waivers require buying within a tight window after your initial trip deposit—usually 10-21 days depending on the insurer. "Cancel for any reason" coverage must be purchased within 14-21 days of your first trip payment. Wait until a month before departure and you're stuck accepting standard terms with more exclusions. This mistake particularly hurts travelers with health concerns who desperately need that pre-existing condition waiver.

Assuming all policies are basically similar leads to inadequate coverage. Policy terms vary dramatically between insurance companies. One might cover trip interruption at 150% of trip cost (letting you buy an expensive last-minute flight home), while another caps it at 100%. One might require 12-hour delays before travel delay coverage starts, another only needs 6 hours. Compare actual policy language, not just premium prices.

Misunderstanding "cancel for any reason" limits disappoints travelers expecting full refunds. This coverage typically reimburses only 50-75% of prepaid expenses, not everything. You'll still lose money, just less of it. Some people buy this expensive upgrade expecting complete protection, then feel cheated receiving partial reimbursement.

Author: Samantha Lowell;

Source: visitmuseumcampussouth.com

How to Decide If Trip Insurance Is Right for You

Answering whether travel insurance makes sense for your situation requires working through a decision framework. This process helps you reach a rational conclusion instead of buying from fear or skipping from blind optimism.

Calculate your financial exposure first. Write down all non-refundable, prepaid expenses: airline tickets, hotel deposits, tour payments, event tickets, cruise fares. This total represents your maximum potential loss if you must cancel. Compare this number to insurance cost. Risking $8,000 while insurance costs $400 means paying 5% to protect 100% of your investment. That usually makes sense. Risking $600 while insurance costs $50 still works mathematically, though the absolute numbers matter less.

Assess personal risk factors honestly. Think about your health, age, and family situation. A healthy 30-year-old with no dependents faces lower cancellation risk than a 60-year-old caring for aging parents. Parents of young children face higher cancellation probability because kids get sick unpredictably. Travelers managing chronic conditions need medical coverage regardless of age. Be realistic about your actual risk profile.

Review existing coverage thoroughly. Pull out your health insurance policy and verify international coverage details. Call your credit card company and document trip protections, including coverage limits and triggering requirements. Check your homeowners or renters insurance for baggage provisions. Create a simple spreadsheet showing what you already have. This reveals actual coverage gaps rather than assumed needs.

Consider destination-specific risks carefully. Research your destination's medical system quality, typical evacuation costs, political stability, and natural disaster patterns. A Tokyo trip requires different coverage than a rural Bolivia adventure. Caribbean travel during hurricane season increases trip interruption risk substantially. Political instability in certain regions might make "cancel for any reason" coverage genuinely valuable.

Evaluate trip timing realistically. How far ahead are you booking? Trips booked nine months out face more cancellation risk than trips booked six weeks out simply because more events can happen in nine months. Consider what might realistically interfere: major work projects, family obligations, health issues, financial changes. Longer booking timelines strengthen the case for insurance.

Factor in trip replaceability. Some trips only happen once. A destination wedding, a milestone anniversary cruise, or a bucket-list African safari might not be easily rescheduled. Other trips—a beach vacation, a city weekend—can happen whenever. The more irreplaceable and time-sensitive the trip, the more insurance makes sense for preserving that specific opportunity.

I tell people to think mathematically, not emotionally. Calculate your insurance cost as a percentage of trip cost, then consider the probability you'll actually need to file a claim. When you're risking $5,000 to save $250 on insurance, you only need a 5% cancellation chance to break even financially. Most people booking six months ahead face higher odds than 5%

— Sarah Chen

Apply reasonable rules of thumb. Insurance costing more than 10% of total trip cost suggests the policy might be overpriced or your trip might be inexpensive enough to self-insure. Insurance costing less than 3% of trip cost probably represents good value. The 4-7% range represents fair pricing for comprehensive coverage on most trips.

Test the "sleep well" factor. After crunching numbers, ask yourself: will I worry about this trip? If anxiety about potential cancellation or medical emergencies will eat at you, insurance provides psychological value beyond pure financial protection. Conversely, if you're genuinely comfortable accepting the risk, skip the coverage and save the money.

Author: Samantha Lowell;

Source: visitmuseumcampussouth.com

Frequently Asked Questions About Travel Insurance Value

Travel insurance works like any other insurance product—it transfers risk you can't afford to absorb yourself to a company that can. The real question isn't whether insurance has theoretical value, but whether it delivers practical value for your specific trip.

Start by running the numbers. Calculate your total non-refundable financial exposure, get insurance quotes from multiple providers, and determine the percentage cost. Most trips fall into that 4-7% range where insurance makes mathematical sense for substantial prepaid bookings.

Then layer in your personal factors: current health status, family situation, risk tolerance, and existing coverage from other sources. A healthy couple with comprehensive credit card benefits and flexible bookings might reasonably skip insurance on a $2,000 domestic trip. A family of four with a $10,000 cruise booked nine months ahead should buy coverage without hesitation.

The value equation balances financial exposure against insurance cost, weighted by realistic cancellation probability and personal risk factors. There's no universal right answer that works for everyone, but there is a rational framework for making this decision intelligently.

For expensive international trips with substantial non-refundable bookings, the answer usually lands on yes. For short, cheap, flexible domestic trips, it usually lands on no. Everything between these extremes requires thinking through your specific circumstances instead of following blanket advice from people who don't know your situation.

Buy insurance when the potential financial loss would genuinely hurt and the premium seems reasonable for that protection. Skip it when you can absorb the loss comfortably or your existing coverage already fills the gaps. That straightforward framework handles most travel insurance decisions without overthinking or overspending.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on travel insurance topics, including coverage options, premiums, deductibles, trip cancellation protection, travel medical insurance, baggage coverage, travel delays, emergency medical evacuation, and related travel protection matters. The information presented should not be considered legal, medical, financial, or professional insurance advice.

All articles and explanations published on this website are for informational purposes only. Travel insurance policies can vary between providers, and details such as coverage limits, exclusions, reimbursement conditions, waiting periods, eligibility requirements, and claim outcomes may differ depending on the insurer, policy type, destination, traveler age, health status, and trip details.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness or reliability of the content. Use of this website does not create a professional relationship. Visitors should review the official policy documents provided by insurance companies and consult with licensed insurance professionals or qualified advisors before making decisions about travel insurance coverage.